30,000 Foot View #5

Four Steps To Start Investing For The Long-term

❗️If you are new here, please consider reading the the first 30,000 Foot View. It was (mostly) written during the COVID-19 pandemic. The uncertainty created by COVID-19 helped to birth that 𝗆̶𝖺̶𝗇̶𝗂̶𝖿̶𝖾̶𝗌̶𝗍̶𝗈̶ first piece of 30,000 content, and that content ties into the topic for today’s edition of 30,000.❗️Start Investing For The Long-term In 4 Steps

✏️EDITOR’S NOTE: If you are new to investing in the public stock market outside of your 401(k), please consider reading this 30,000 foot introduction. If you are 𝖺̶ ̶𝗆̶𝗂̶𝗇̶𝗂̶𝗈̶𝗇̶ ̶𝗈̶𝖿̶ ̶𝖣̶𝖺̶𝗏̶𝖾̶𝗒̶ ̶𝖣̶𝖺̶𝗒̶ ̶𝖳̶𝗋̶𝖺̶𝖽̶𝖾̶𝗋̶ someone that has already starting invested outside of your 401(k), skip down to the COVID CAPITAL section.

In a modern world filled with pitfalls, everyone strives to live in the moment, to not dwell so much about the past, and to not worry too much about the future. But the best example of when that sage advice does not work is when it comes to investing. Particularly, if the time horizon of the investment is long-term.

When investing you are inherently looking into the future. Or trying to anyway. Remember what the goal is when you “invest” in something. You are simply anticipating that the asset you are investing in will likely be worth more in the future than it is today.

While 30,000 #1 & #2 very much focused on basic personal finance and the theoretical fundamentals long-term investing, the actual initial steps of how to start investing in the public stock market for the long-term were not specifically tackled.

📖 Scenario: for most people as you start getting your personal finances in order—you are likely between 30 to 40 years old, and you are making an annual salary or total annual wages of between $50,000 and $100,000. Yes, that’s a big range. But, that’s the point. These initial steps are nearly universal. If you are younger, great! If you are making more money, fantastic!

The list is a total of four steps. Step that almost anyone can take without spending a lot of time or even a lot of money. This is 101 stuff. The basics. A, yes, true 30,000 foot view. It’s about getting started. So lets do just that—get started.

1️⃣. Take responsibility for your personal finances, creating a savings plan inclusive of stock market investing.

This was the topic of 30,000 #2. We should all know our individual P/L (profit and loss) on a monthly basis. Sadly, I think a lot of people do some of the additional steps listed below without really owning this important first step. That can work for a while, especially when times are good, but it might not work forever.

There’s even a simple spreadsheet to get you started in #2 if you’d like to analyze your income and expenses.

The desired outcome of this work is to know; (1) what you are currently saving, and (2) whether or not you can increase that savings rate on a weekly/monthly basis.

2️⃣. Maximize your company’s 401(k) match and work towards hitting the 401(k) limit.

If your company matches up to a certain percentage of your salary/wages, make sure you are getting that free money by contributing at least that percentage to your 401(k) annually.

The 401(k) limit for 2020 is $19,500 (for most people). Many advisors would say you are doing something wrong if you are not hitting that limit.

Yes and no. First, not everyone can afford to save nearly $20,000 in a given year. Moreover, while some people chose to use their company’s 401(k) as their only savings instrument, others might be saving and investing via other vehicles.

Go back to your P/L analysis. Make sure you are at least working towards hitting this limit, e.g., as your salary/wages increase, you should also increase the percentage you put in your 401(k) and other savings instruments. No exceptions. If you are not saving $20,000 annually, make meaningful strides each year. Then, once you hit that…keep going!

3️⃣. At the same time as step 2 above; open an individual brokerage account or an individual retirement account (IRA).

Either account type works. What matters is that you start learning. Potential vendors include Charles Schwab, E*TRADE, Fidelity, and TD Ameritrade. Again, this is not important right now. Do what is easiest, i.e., use a vendor that you already have a relationship with, if applicable.

Back to the type of account question; if you are in the, say, $50,000 - $100,000 income range I would not do an individual brokerage account nor a traditional IRA. I would consider a Roth IRA if you are willing to do a little extra research. More on that some other time.

4️⃣. Buy low fee¹ funds in said account. Do this each and every week or each and every month.

You can start with as little as a few dollars a month theoretically. If you are on the lower end of our hypothetical income range, try to do at least $80 a month. Why $80? That would be approximately $1,000 invested over one year. Also, think about what eighty-bucks represents to you … $80 per month is comparable to what you might pay for streaming services, a cell phone bill, internet access, gym membership/workout classes, etc. so treat this as money that automatically comes out of your income. It’s no longer yours. It belongs to the market now!

In future years, when you revisit Step 1, dedicate a portion of any incremental income to not only your 401(k) but also this second individual account.

Okay, now what to buy in this individual account:

S&P 500 — ticker: SPY

SPY is an example of an exchange traded fund (ETF). The S&P 500 is the best representation of the overall stock market. It is an index of companies inclusive of organizations of all sizes, across all industries. There are many companies you know—Apple, Alphabet (that’s Google), Berkshire Hathaway, Facebook, Johnson & Johnson, Microsoft, Nvidia, Pfizer, Verizon, Visa, Wal-Mart, etc.

Buying SPY is the simplest thing you can do. When to hear words like “low cost index fund” or "low cost mutual fund” or “low cost ETF” — that’s SPY. SPY gets you in the market. It gets you in the game.

That said, I can’t help but offer an alternative² that is slightly more complex below. I think it’s worth the read but if you are feeling overwhelmed, it’s not required.

Nasdaq 100 — ticker: QQQ

QQQ is another ETF. The Nasdaq 100 is a basket of companies of which, once again, you have probably heard of many—from Amazon, Activision-Blizzard, Costco, Kraft Heinz, Netflix, PayPal (which also owns Venmo), Starbucks, and so on. As you might notice from this partial list, it’s a “tech” heavy basket but, as you can see, has other traditionally “non-tech” names, too.

Just four steps, and two funds. This could be accomplished over the course of a week.

After your company 401(k) and this new individual account have an accumulated value of, say, 0.5-1x your annual salary—then you can consider allocating a small percentage of your hard-earned investing dollars to other ETFs or even individual stocks if you are willing to put in the work of researching them.

In my opinion, there are a whole bunch of (more fun) things to think about as you broaden your investing portfolio. For others, they could care less. The four steps above will serve those people well. For those that would like to start analyzing sectors, industries, and individual companies; there are examples in the COVID CAPITAL section below.

Part 2 — continuing to disclose individual stock purchases since COVID-19 hit the US and impacted the stock marketLast time the financials were the topic of conversation. This time we will go across a few industries. Namely — Media/Entertainment/Communications, Energy/Utilities, and Aerospace/Defense/Industrials

Here are the purchases during COVID:

Note: the only timing exception is GE, which was not purchased during COVID-19. It is a relic from the past. And I mean that in so many ways. :(

🔩Industry/Sector: while we are going across three sectors with this list, many of the companies above actually share more in common than one might initially think. In fact, with the exception of Disney and ViacomCBS, the balance of the companies above are the epitome of “value” stocks in 2020. And boy have they been unloved while the market fawns over a few large high-tech companies. That has meant there was a significant opportunity to buy these companies, and others like them, at a historical discount in March. A couple examples are provided below.

📈Short-term Performance: The company I will first call out here in illustrating short-term performance is UPS. It’s a boring industrial company, right? Well, this company, and its peers, remain quite important in 2020. When UPS reported earnings last month, the market had a strong reaction. I took a screen shot on that evening:

It’s not easy to move a $125B market cap company 14% in day. It’s even harder to move an “old school” industrial company 14% in a day, especially considering it was already nearly recent highs.

The broader point here; there is serious potential value in many of these names whether they are “sexy” companies or not. And that value is not just in the dividends paid by most of the companies on this list. That said, for UPS, even at these price levels, it yields nearly 3%.

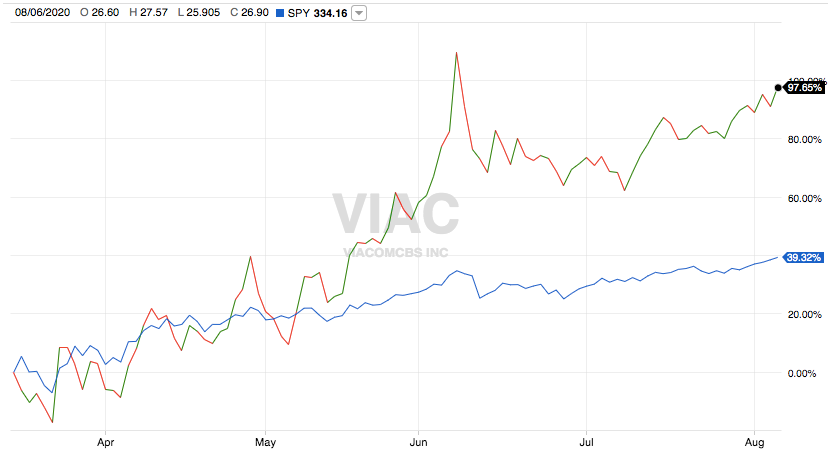

Speaking of hunting for value, the aforementioned ViacomCBS is also an interesting 2020 case study. It’s very different than UPS in all manners. Even before COVID, it had internal management problems that made it unloved. There are also varying opinions on how it fits in to the ever evolving media landscape.

Most of all, ViacomCBS in 2020 has illustrated a couple of things: (1) the opportunity presented by COVID-19 as stocks that were already unloved and discounted plummeted to unsustainable low levels and, (2) that entry point into individual stocks matters. In fact, you might call that the paramount tenet of “value investing” if there is one.

Example 1: Early March entry point into VIAC = 10.6% return

Example 2: Mid-March entry point into VIAC = 97.7% return

Both outcomes are not bad, but they are certainly not equally good.

✏️EDITOR’S NOTE: You were spared any discussion of the “boring” energy and utility companies listed above. Instead you got the dynamism of a UPS and ViacomCBS. But we cannot help ourselves. Consolidated Edison announced its quarterly earnings as this article was being polished and finalized on August 6th. No one batted an eye. Crickets. Amidst the chaos of 2020, ConEd’s earnings grew year-over-year. Forward guidance was reaffirmed. Forward guidance! Who even does this guidance stuff?! The stock continues to yield above 4% and the company’s cash flows remain healthy. It’s very likely it, and others like it, will have a moment in the sun someday. Until then, we are paid to wait.

FOOTNOTES:We are not even going to get into fees here. If you would like to do some research, look into expense ratios of ETF and mutual funds. Here’s my summary … If you are brand new to investing in the stock market, why would you pay a fee to invest in a fund you do not understand? You do not want to beat the market. The goal starting out is to be in the market.

Alternative: you can buy SPYV which is a subset of SPY. It includes larger, well established companies that (mostly) pay a dividend. If you not familiar with dividends, you needn’t worry or research. These companies generally have more stable revenues and conversely have a more stable stock price. Examples include; Johnson & Johnson, Pfizer, Verizon, and Wal-Mart.

If you buy SPYV, you should also buy SPYG which are companies that are typically growing revenues year-over-year. Because growth is hard to come by and introduces new risks, these companies have revenue streams that are less certain and thus stock prices that can fluctuate (up or down!) more significantly relative to the companies in SPYV. Examples include; Apple, Alphabet, Facebook, Microsoft, Nvidia, and Visa. If you chose this alternative SYPG and SPYV approach, that means you take the weekly/monthly value you want to invest (i.e., the $80 mentioned above) and split it equally between SPYV and SPYG. An additional benefit is if your account does not let you purchase fractions of shares, SPYV and SPYG are less expensive on a per share basis.